The postings on this site are my own and do not necessarily represent the postings, strategies or opinions of my employer.

- On LLM Series.

- On Cloud Series.

- On Platformization of Banking Series.

- AI and Data: The Powerhouse for Banks

- Reimagining Recommendations: LLMs as a New Frontier (LLM Part 12)

- Uplift Bank Profits. AI to Maximize Customer Lifetime Value (Product Holding Ratio). (LLM Part 13)

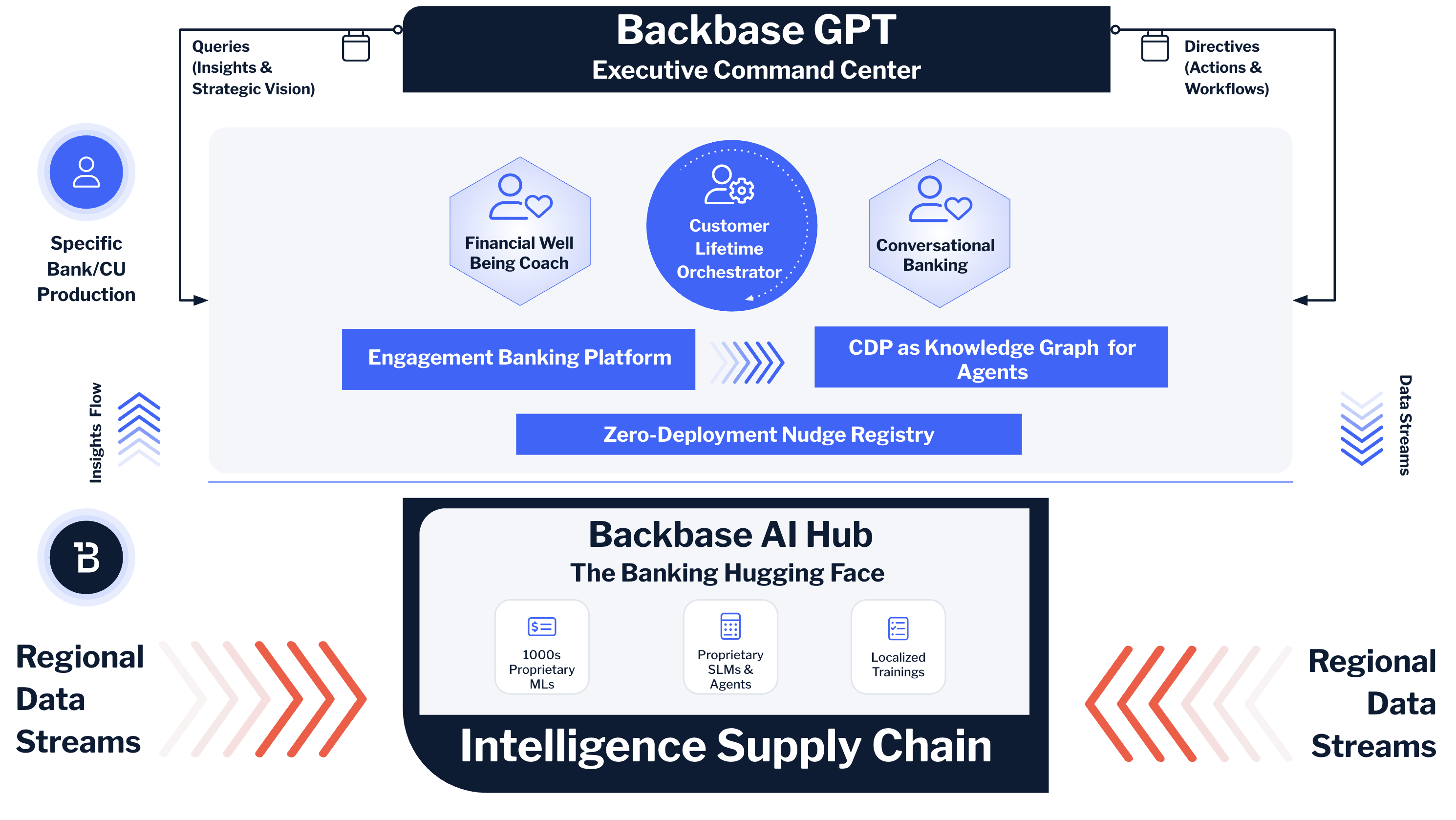

- AI-Driven Customer Lifetime Orchestration for Banks (LLM Part 14) - This is co-authored with Quynh Chi Pham and Amelia Longhurst .

The Imperative for Customer Lifetime Value (CLV) Optimization

Banks today face mounting pressure to enhance profitability while navigating increasing competition and evolving customer expectations. Maximizing CLV is critical by increasing product holding ratio, but traditional approaches struggle to deliver the necessary personalization and proactive engagement.

The product holding ratio refers to the average number of products or services a customer uses from a bank. A higher product holding ratio generally indicates a stronger customer relationship and a higher CLV. Here's why:

- Increased Revenue per Customer: Each additional product a customer uses generates more revenue for the bank through fees, interest, or transaction charges.

- Stronger Customer Relationships: Customers using multiple products have more touch points with the bank, leading to deeper engagement and stronger relationships; also lower costs of marketing.

- Reduced Churn: Customers with multiple products are less likely to switch to a competitor because it's more inconvenient to move multiple accounts and services.

- Cross-selling and Upselling Opportunities: Customers with multiple products are more likely to be receptive to cross-selling and upselling offers for other relevant products.

For instance,

A customer who only has a basic checking account generates revenue primarily through transaction fees (if any) and potentially through the interest earned on the deposit balance (which is usually minimal). Their CLV is relatively low.

Generates $50 in annual revenue. Stays with the bank for 5 years. Simple CLV calculation = $250.

A customer who has a checking account, a savings account, a credit card, and a mortgage generates revenue through multiple channels:

- Checking account: Transaction fees (if any).

- Savings account: Interest earned on deposits.

- Credit card: Interchange fees, interest on outstanding balances.

- Mortgage: Interest payments.

This customer's CLV is significantly higher due to the multiple revenue streams and their increased stickiness to the bank.

Generates $500 in annual revenue. Stays with the bank for 10 years. CLV = $5000.

By intelligently recommending and facilitating the adoption of additional products and services relevant to each customer’s unique needs, this orchestration strategy strengthens customer relationships, increases revenue per customer, and significantly reduces churn.

This post presents AI-Driven Customer Lifetime Orchestration, a transformative solution that leverages the power of artificial intelligence (Gen AI and ML) to create personalized 90-day plans for each customer and each product. These plans are strategically designed to increase product holding ratios, a proven driver of CLV.

The Challenge: Maximizing CLV in a Dynamic Market

In today's rapidly evolving financial landscape, maximizing CLV presents a significant challenge for traditional banks. The market is no longer defined solely by established players; the rise of agile adoptions, fintechs, strong modernized banks has intensified competition, forcing established institutions to rethink their customer engagement strategies. These new entrants often excel at providing seamless digital experiences and personalized services, raising customer expectations across the board. Customers now demand banking interactions that are convenient, intuitive, and tailored to their individual needs, putting pressure on banks to modernize their offerings and deliver comparable digital experiences.

One of the core difficulties in maximizing CLV lies in effectively engaging customers across the expanding array of available channels. Customers interact with banks through various touchpoints, including branches, ATMs, online banking, mobile apps, and contact centers. Maintaining a consistent and engaging experience across these fragmented channels is a complex undertaking. Siloed data, disparate systems, and traditional marketing approaches often hinder banks' ability to deliver personalized communications and targeted offers at the right moment, leading to missed opportunities for deeper customer relationships.

Furthermore, optimizing product holding ratios remains a persistent challenge. Traditional cross-selling and upselling techniques often lack the necessary personalization and relevance to resonate with today's digitally savvy customers. Banks need a more intelligent and proactive approach to identify customer needs and offer relevant products and services at the right time. This dynamic environment necessitates a shift away from reactive, product-centric strategies towards a proactive, data-driven approach to customer relationship management. Banks must embrace innovative solutions that enable them to truly understand their customers, anticipate their needs, and orchestrate personalized journeys that maximize long-term value.

Introducing AI-Driven Customer Lifetime Orchestration: A Strategic Approach

AI-Driven Customer Lifetime Orchestration represents a paradigm shift in how banks approach customer relationship management. It moves beyond reactive, campaign-based interactions to a proactive, continuous, and highly personalized approach to managing the entire customer lifecycle. This strategic approach leverages the power of artificial intelligence to anticipate customer needs, orchestrate relevant interactions across all touch points, and ultimately maximize CLV. Unlike traditional CRM systems, which primarily focus on managing customer data and interactions, AI-driven orchestration actively manages the customer journey, guiding customers towards relevant products and services at the right time and right context.

Traditional marketing automation, while valuable for automating marketing campaigns, often lacks the deep personalization and real-time adaptability of AI-driven orchestration. Marketing automation typically relies on pre-defined rules and segments, whereas AI dynamically adapts to individual customer behavior and context. AI-driven orchestration uses advanced analytics, machine learning, and predictive modeling to understand each customers unique journey, identify opportunities for engagement.

The strategic value proposition of AI-driven Customer Lifetime Orchestration lies in its ability to proactively manage the customer lifecycle and maximize CLV. By orchestrating personalized 90-day plans (as discussed later), banks can move beyond simply reacting to customer actions and instead anticipate their future needs. This proactive approach allows banks to:

- Increase customer engagement: By providing relevant and timely information, offers, and support.

- Improve product holding ratios: By intelligently recommending and facilitating the adoption of additional products and services.

- Reduce customer churn: By proactively addressing potential issues and providing personalized retention offers.

- Enhance customer satisfaction: By delivering seamless and personalized experiences across all channels.

The Backbase Customer Lifetime Orchestrator begins by deeply understanding your product portfolio and their respective Customer Value Propositions (CVPs) as well as marketing branding guidelines for your bank and if any product specific across all categories. This foundational step is crucial for proactively orchestrating ongoing customer engagement.

Based on your specific objectives—such as NTB onboarding within 90 days, driving wealth product adoption among affluent customers, or maximizing credit card EMOB— our AI Agent Customer Lifetime Orchestrator generates optimized 90-day plans. These plans leverage customer engagement data from our embedded CDP, including login history, financial behavior, and product holdings. Importantly, our AI agents continuously learn and refine plan generation based on its past performance, ensuring ongoing optimization and self-learning.

Beyond plan generation, our AI agents create the marketing assets needed to engage customers across all channels and retargeting —from images to compelling content.

Our AI agents take a data-driven approach to marketing, generating channel-specific materials designed to maximize customer reach. Built-in self-learning and split testing capabilities allow these agents to constantly optimize content and improve campaign results.

Following the execution of these activities, an executive dashboard provides a comprehensive view of product holding ratio performance, enabling executives to stay informed and make data-driven decisions.

This executive dashboard provides a comprehensive, at-a-glance view of key performance indicators related to customer engagement and product adoption. By consolidating critical metrics such as total retail customers, new-to-bank (NTB) customer acquisition, 90-day active NTB customers, average product holding per NTB customer, average deposits, transaction volume and value, and customer interactions, executives gain immediate insight into the effectiveness of customer lifetime orchestration strategies. The inclusion of trend charts over a 90-day period allows for easy visualization of progress, identification of growth areas, and timely detection of potential issues. This data-driven approach empowers executives to make informed decisions, optimize resource allocation, and ultimately drive sustainable growth in customer lifetime value.

The dashboard includes a suite of pre-built Early Warning Indicators (EWIs) that provide predictive insights into critical areas such as potential declines in CASA balances and upcoming credit card renewals, allowing for proactive mitigation strategies.

Quantifiable Results: Driving Revenue and Profitability

AI-driven Customer Lifetime Orchestration offers a clear path to measurable improvements in key financial metrics, directly impacting a bank's bottom line. By focusing on increasing customer engagement and product adoption, this approach delivers quantifiable results across several crucial areas. One of the most significant impacts is seen in the average product holding ratio. By intelligently recommending relevant products within personalized 90-day plans, banks can expect to see a substantial increase in the number of products each customer uses.

This enhanced product adoption has a cascading effect on customer retention rates. Customers with multiple product relationships are significantly less likely to switch banks due to the increased inconvenience and the deeper integration with the institution. Studies have shown that customers with three or more products have a significantly higher retention rate (often exceeding 90%) compared to single-product customers. This reduction in churn directly contributes to CLV growth.

For example (real bank information is anonymized and numbers are changed),

A bank has 1,000 NTB customers. Before implementing the orchestration strategy, they hold 1500 products in total. The average product holding ratio is 1.5. After implementing the 90-day plans, these same customers hold 1800 products. The new average product holding ratio is 1.8, a 20% increase. This increase translates to more revenue streams per customer. If each additional product generates an average of $100 in annual revenue, this 20% increase in product holding ratio leads to an average revenue increase of $30 per customer per year.

Without the orchestration strategy, they lose 800 of these customers within the first year (80% churn). With the orchestration strategy, they only lose 200 (20% churn). The retention rate improves from 20% to 80%.

A more accurate CLV calculation considers discount rates. A simplified formula is:

CLV = (Average Annual Revenue per Customer * Gross Margin) / (Discount Rate + Churn Rate)

Let's assume:

- Average Annual Revenue per Customer: $500

- Gross Margin: 50%

- Discount Rate: 10%

- Churn Rate (without orchestration): 80%

- Churn Rate (with orchestration): 20%

- CLV (without orchestration): ($500 * 0.50) / (0.10 + 0.80) = $277.78

- CLV (with orchestration): ($500 * 0.50) / (0.10 + 0.2) = $833.34

This shows a 200.7% increase in CLV due to reduced churn. If we combine this with the increased revenue from a higher product holding ratio, the CLV improvement becomes even more significant.

If a bank has 10,000 NTB customers and increases the average revenue per customer by $30 (due to increased product holding) and reduces churn from 30% to 5%, the impact is:

- Increased Revenue: 10,000 customers $30/customer = $300,000 per year.

- Cost Savings from Reduced Churn: Assuming an acquisition cost of $200 per customer, reducing churn by 5% saves the bank $100,000 (500 customers $200).

- Combined Impact: The total financial benefit in this scenario is $400,000 per year.

Conclusion

For bank executives seeking to drive substantial growth in CLV, enhance customer loyalty, and optimize product adoption, AI-driven Customer Lifetime Orchestration offers a compelling solution. The combination of personalized 90-day plans, powered by sophisticated AI Agent algorithms, and a comprehensive executive dashboard provides the tools and insights necessary to achieve these critical objectives. This data-driven approach translates directly to increased revenue, improved profitability, and stronger customer relationships, positioning banks for long-term success in the digital age.